By Rich Harvey, CEO & Founder, propertybuyer.com.au

There’s a little panic seeping into Sydney and Melbourne’s property markets. Interest rate rises, increasing cost of living, Federal election paralysis and ongoing international challenges have converged to put the brakes on our extraordinary price growth.

This presents a quandary for owners, especially recent buyers. They’re asking themselves whether it’s smart to take the profit (or stem future losses) by selling out now, or hold firm wait for things to turn around.

First, let me say that whatever move you decide to make should be based on your own personal circumstances. That said, throughout my years of experience I’ve seen the real money made not in selling too soon, but by holding for the long-term.

Here’s why staying the course should be your first instinct.

Principles of wealth

There are some fundamental principles which ensure you make the most impressive gains from long-term real estate ownership.

Firstly, property prices move in cycles – but they aren’t those even up-and-down waves you used to see in science class. Rather, markets over the long term tend to rise, then fall modestly to a plateau before rising again.

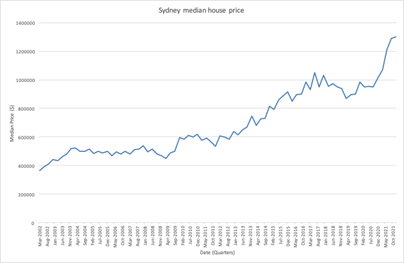

To illustrate, here’s a chart of Sydney’s quarterly median house price from March 2002 to October 2021:

(source: ABS)

(source: ABS)

You can clearly see the way house prices have moved. None of the troughs plough too far below the previous peaks. This graph demonstrates the huge benefits in capital gains enjoyed by those who hung tight rather than cut and run early.

The second principle delivering long-term upside is compounding. By not selling your property, you are effectively reinvesting your capital gains back into the market which sees your asset’s value compound at an exponential rate.

For example, let’s say you invest $500,000 in a property that increases in value by five per cent per year on average. Year one, the property is worth $525,000. That amount then increases by five per cent in year two to reach $551,250. Same for year three to reflect $578,800, and then year four when it will value at $607,750.

Notice something? You aren’t just earning five per cent on your original $500,000, but also on your progressive gains.

And the longer you hold the property, the more impressive those gains are. In the above scenario if you held a $500,000 property for 15 years, it’s market value would be just shy of $1 million.

In fact, if you invest in the right type of property and location, you can expect to see its value double every 10 to 15 years. That’s not too bad – especially when the bank is financing most of those gains (but perhaps leveraging is a discussion for another blog).

And this doesn’t account for added benefit of rental income. At present, vacancy rates remain incredibly low. Tenant demand for your property is at an all-time high right now which means you can maximise rent.

To draw on an adage, it’s better to shear the sheep than kill the herd when it comes to getting the most out of your property investing.

But isn’t the current price a market peak?

I can see some owners and investors would still be thinking that surely if prices are peaking, now is the time to sell out and perhaps invest elsewhere.

The challenge with property is that selling requires time and money. It can take you several weeks – sometimes months – to list, market and sell a property. You will be responsible for advertising costs, agents commission and other professional fees. In addition, you could be up for other charges, taxes and levees too.

These costs can be expensive and must be factored into your decision making, especially if you’ve only owned the property for a few years. It will normally be more prudent to simply park the investment and let it ride the next wave of capital gains.

The secret to making it work

One fundamental that improves the upside of a long-term holding is buying the right home or investment in the first place.

If you choose wisely, you will acquire an asset that remains in high demand for years to come. You’ll be well positioned to get the best value uplift and, for investors, a strong rental return helping you service the debt.

As Albert Einstein famously said “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn't … pays it.”

The best way to ensure you find these golden opportunities is by relying on a qualified buyers’ agent.

We understand our markets and our client’s needs. We are also skilled at securing a property for you at the best possible price, so you can enjoy all the upsides of long-term ownership.

To have one of our friendly Buyers' Agent's contact you, click here to:

or

or

call us on 1300 655 615 today.

.svg)

.svg)

.svg)