By Guest Blogger, Pete Wargent,

Next Level Wealth - www.gonextlevelwealth.com.au

Easing cycle

It’s well known that housing is one of the most interest rate sensitive sectors of the economy.

But if you think about how long the property buying process takes, then it’s reasonable to expect that it also typically takes time for the market to adjust to interest rate changes.

The boffins may tell you that it takes 18 months for the full impact of an interest rate cut to flow through the economy.

This may be technically true.

But we also know that property markets are fragmented, and sentiment driven.

And experience on the ground and at auctions has shown us that the impact on property market confidence of an interest rate cut can sometimes be almost immediate.

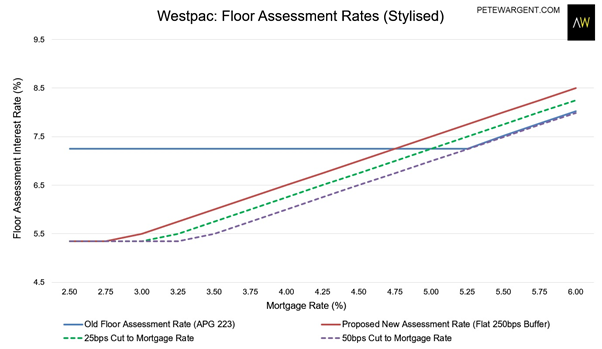

Serviceability changes

It’s not just interest rates that determine your borrowing capacity but also serviceability restrictions.

Without getting too technical, when you borrow a mortgage the bank must stress test the transaction to ensure that you can pay back the mortgage if interest rates move higher.

Earlier this year the advisory floor assessment rate of 7% (banks were generally using 7.25 per cent) was removed and replaced by a 250-basis points buffer.

In plain English, you need to able to afford the repayment if the mortgage rate increases by 2.5 per cent.

We did some detailed work on the impacts of this change at the time.

And our findings were that while the initial impacts would be modest, if mortgage rates were to fall as expected towards 3 to 4 per cent then the impact would be magnified.

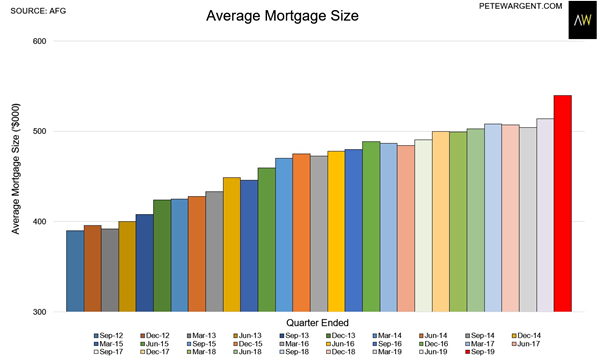

Rates fall again

In the event, the expected interest rate cuts did happen, mortgage rates fell, and so this led in many cases to an increase in borrowing capacity of about 15 per cent.

And when Aussies are offered more borrowing capacity they generally use it, so you should be able to guess what happened next.

Yes, you guessed right!

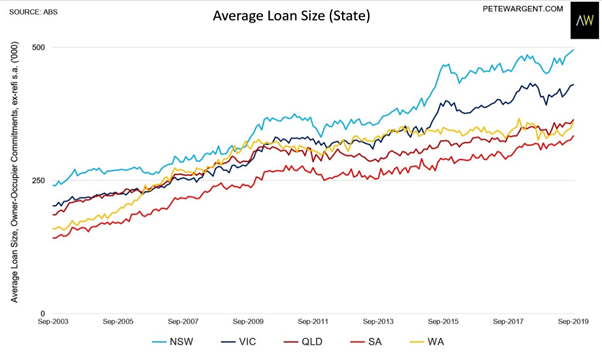

As we already noted, markets are fragmented and move in their own cycles.

All available figures show that mortgage sizes in New South Wales have jumped higher in response to the changes, so expect Sydney housing prices to follow.

Other markets such as Brisbane didn’t experience too much of a downturn, and as such have returned to steadier growth.

The chart below from the ABS shows the average new homebuyer loan size by state.

The mortgage aggregator Australian Finance Group (AFG) runs a similar series, and it also found a surge in loan sizes in New South Wales to a record high.

Is there a clear link between interest rates and potential for capital growth?

Certainly at the macro level housing has generally responded noticeably to interest rate cuts.

But at the micro level, factors such as scarcity value in property selection will always be important.

To have one of our friendly Buyers' Agents to contact you in regards to buying property :

or

or

call us on 1300 655 615 today.

.svg)

.svg)

.svg)