By Rich Harvey, CEO & Founder, propertybuyer

Written by: Rich Harvey, CEO & Founder

propertybuyer.com.au

Click here to watch Rich's Video of the July Market Update:

Many buyers are watching the media headlines - property prices falling / the average consumer in Australia is not feeling very confident about their economic future. Rapidly rising inflation figures, recent interest rate rises and loss of confidence in the global markets have really taken a toll in the mind of consumers as they reassess the family finances.

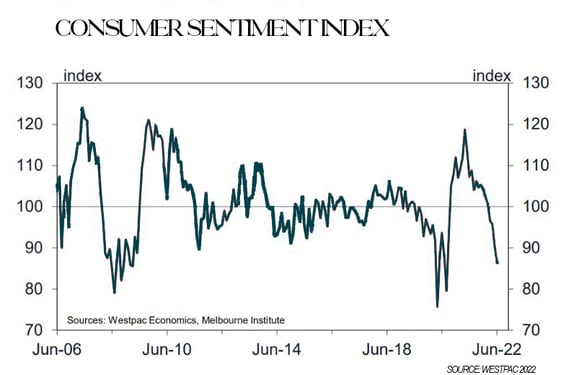

Consumer sentiment as measured by the Westpac Melbourne Institute has slumped dramatically, falling 4.5% in June to 84.6, from 90.4 in May.

Westpac report that over the 46-year history of the sentiment survey, they have only seen Index at these record low levels during previous major economic dislocations including COVID-19 (75.6), the Global Financial Crisis (79.0) and the early 1990s recession (64.6); the mid-1980s slowdown (78.7) and the early 1980s recession (75.5). Chief Economist Bill Evans at Westpac notes that those last three episodes were associated with high inflation; rising interest rates; and a contracting economy – a mix that may be threatening to repeat.

Feelings aren’t facts.

Consumer sentiment simply measures what people feel about the economy and the economic outlook both here and abroad. Living on a diet of negative media news will undoubtedly lead most consumers to have a negative outlook.

But let’s take a step back from the pessimistic perceptions and take a deeper look into the current economic headwinds and tailwinds and look at what is likely to eventuate over the next 12 to 18 months.

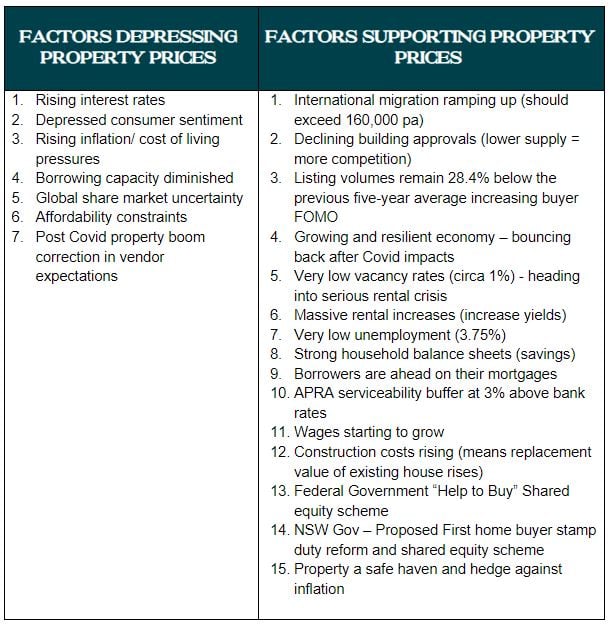

I sat down the other day, put on my thinking cap, and wrote down all the factors that were dragging the property market down vs all the factors that were driving it up. Here’s what I uncovered:

I am sure you can add more factors to each side of the ledger - we all have a natural bias in the way we think things will turn out. Some factors are more important than others will have more influence on market direction. But there are several important takeaways of serious note.

-

Interest rates are just one factor among many – interest rates are still very low and are normalising to counteract rising inflation. I expect the cash rate to settle somewhere in the 2% to 2.5% range in the next 18 months. This will result in the average mortgage rates being around 4.5%. The RBA cannot raise rates nearly as fast as they reduced them as we have much greater leverage (borrowings) in the economy. The interest rate lever is now more sensitive for the average consumer.

-

Despite declining consumer sentiment, the economy is not collapsing. In fact, the RBA in its latest economic statement said that GDP growth is on track for 4.25% increase to Dec 2022 and then 3% to June 2023.

-

We have a very strong labour market with unemployment rate at record lows of 3.75% and wages starting to rise.

-

Counteracting the rising borrowing costs for home buyers and investors is the rapid rise in rents. CoreLogic report a 9% increase in rents so far this year and I expect to see rents continue to rise – good news for investors, but challenging news for renters.

-

The Westpac Melbourne Institute also produce a “Time to buy a dwelling” index of House Price Expectations fell by 8.4% from 121.4 to 111.1. Westpac Chief Economist Bill Evans points out the index is still above 100 overall, indicating that more consumers expect prices to rise than fall. In NSW the Index fell by 11.2% to 103.8 while in Victoria it fell by 9.9% to 101.50. In Queensland the index rose 3.1% to 124.5 indicating greater optimism on property prices in the sunshine state.

-

Markets tend to overshoot or undershoot based on expectations. The trick for savvy home buyers and investors is to take a long-term view.

-

Corelogic data is backward looking and typically 2-3 months out of date – market conditions change much faster on the ground that what is reported in the media. For example, the current figures for the CoreLogic daily home value index suggest that prices in Sydney have declined 2.7% for the quarter. However, on the ground, we are already seeing prices coming back 10% in several areas.

-

Put property price declines into perspective - read the facts not just the headline.

A 1% fall in prices per month is not a crash after a 30% increase during Covid.

-

Property owners are staying in their houses longer – aging in place and avoiding the excessive stamp duty impost.

-

There is not ONE property market - market forces are very localised.

-

There is not ONE property type.

-

There is not ONE property cycle.

-

So, the message here is that once prices stabilise and find a new plateau, this will not be picked up in the official figures for 3 to 5 months down the track. The next 6 months will provide some of the best buying opportunities we have seen (similar to the serious negative sentiment we saw just after Covid hit (March 2020- June 2020) and the GFC in 2008 (I bought three properties that year myself).

The conditions for buying property have now swung in the buyers’ favour – there’s so much less competition out there, auction clearance rates have declined, and vendors are more negotiable – but you still need to be careful with your property selection and offer pricing.

If you’re trying to work out when is the best time to buy, then please feel free to reach out for a friendly conversation with my team of buyers’ advocates.

Click here to get in touch with the Propertybuyer team:

or call 1300 655 615

.svg)

.svg)

.svg)