By Guest Blogger, Pete Wargent,

Next Level Wealth

How much is enough?

When it comes to thinking about how much passive income, you'd really like without having to work, or what level of income you'd like at retirement, most people have no idea on how to calculate the figure or have limited ideas on how to take the wealth creation steps to get there.

Usually when you ask people, they pick a round figure such as $100,000 per annum, or sometimes $150,000 per annum, but without a whole lot of thought as to why, or how they might get there.

Let’s take a look at this today and consider how a property portfolio might help you to achieve your goals.

The 4% rule

There was an old rule of thumb, originally devised in the 1970s, known as the 4% rule, which suggested that if you withdraw 4% of your portfolio in year one, and increase the annual withdrawals each year, to account for inflation, then in most scenarios your portfolio will last you through at least three decades of retirement.

This in turn suggests that liquid assets of around $2.5 million to be invested in equities might be enough to generate a passive income of $100,000.

There are many possible nuances here.

What if the market crashes in year one or two, for example? Can you adjust your spending accordingly and reduce the withdrawals?

To generate passive income from a property portfolio is a different equation.

Most often rental yields from residential property are relatively low, and there are always holding costs to account for in the form of rates, repairs, vacancy periods, insurance, property management fees, and more.

For these reasons, generating passive income solely from a residential portfolio is usually a long, hard slog.

To account for this, many portfolio investors in real estate aim to reduce debt later in the journey by paying down their mortgage balances, perhaps through selling a property or two in the portfolio, while others might tilt towards commercial property (an industrial unit might be able to generate a net rental yield of 6-8 per cent, for example).

A different way to think about achieving passive income

In reality it’s often hard to know what the ‘end game’ might look like for property investors who are at an earlier stage of their journey.

For this reason, it’s often better to focus on growing as much equity or net worth as possible across your property portfolio, which will give you an attractive range of choices when it comes to transitioning the retirement or passive income phase.

For example, if you can build a property portfolio worth $5 million over time, with $2 million of investment mortgage debt, then you will have equity of $3 million in the portfolio.

This presents you with some choices as to what you might look to do next, in terms of converting the equity into a passive income stream, either from commercial property, equities, or other asset classes such as annuities or fixed income investments.

We often hear people saying “it would be great to own a couple of investment properties one day” but they don't take the proactive steps to actually buy the first property.

Retirement for people just seems too far away, and they fall into a false sense of security thinking that as time goes on that I'll be able to achieve their wealth goals by magic.

Being a procrastinator won’t help you obtain a high passive income, nor will it adequately prepare you for a safe and secure retirement.

The best time to start when it comes to building a property portfolio is usually today, to give yourself the longest possible runway to benefit from compounding capital growth.

The pension conundrum

The Age Pension in Australia is currently a little over $1,000 per fortnight for a single person, or $1,600 per fortnight for a couple.

In other words, it’s not much to live on, especially given the way rents and the cost of living in Australia have gone over recent years.

This is why people look to build up a pension in their superannuation fund, or through a property portfolio, for example.

I’m often asked to calculate the right number of properties to buy to achieve a $100,000 or $150,000 passive income.

I’d argue it’s more important to focus on the quality and value of your assets rather than quantity of properties.

You could buy 30 cheap or poor-quality properties, which might make for an interesting brag at a barbecue, if that’s your sort of thing.

In my experience, however - and speaking as someone with a large property portfolio - these types of assets are often more trouble than they are worth, creating ongoing headaches and costs in the form of time, worry, tenant problems, unpaid rents, and expenses.

Managing a large portfolio of poor-quality properties can be more stressful and more time-consuming than having a job, and the income generated is usually far from ‘passive’.

When calculating a target portfolio and net worth, focussing on the value of your assets and mortgage debt rather than the number of properties is often a better way to think.

What about debt?

It’s both normal and sensible to have a healthy fear of mortgage debt.

What mindset do you need to adopt in order to think about buying an investment portfolio, and not get worried about debt and interest rates?

The first thing to note is that if you’re going to invest over long periods of time – say, a few decades – there will be periods of rising and falling interest rates, recessions and booms, periods of overbuilding and undersupply, and so on.

Market cycles are a feature of all asset classes, not a bug, and often the best investments are made at times when sentiment is at its lowest.

We’ve just been through the fastest tightening cycle for monetary policy in modern history, with 400 basis points of interest rate increases delivered in rapid-fire manner.

The world has far from ended, but it has certainly created some stress and pain in the housing market.

Looking further ahead, interest rates will likely be on their way back down in 2024 and 2025.

I’ve always felt that one of the neatest things about property as an asset class is that you don’t need to put nearly as many of your own dollars into the investment to build a very large portfolio.

It’s true that this requires some smart decisions are careful management of debt and risk.

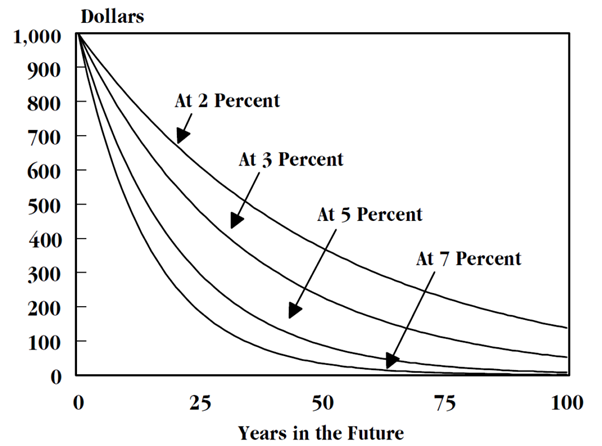

But over time you’ll find that even very large mortgage balances are steadily inflated away.

My wife Heather rarely tires of telling me how her first mortgage was around £60,000 ($120,000), a crippling sum of money at the time which required lodgers to help her make the repayments, and yet a figure that 3 decades on you could feasibly bung on a couple of credit cards.

Meanwhile even modest capital growth of 4-5% per annum can create spectacular results for you over long periods of time.

Real estate is on only asset class where everyday individuals can borrow large sums of money, for very long periods of time, and at comparatively low interest rates…and without a high risk of the loan being called in by the lender.

Once you understand the time value of money, you may well consider many financial decisions differently, from student loans to car purchases, wedding costs, home renovations, holidays, school fees, pension contributions, and more.

Overcoming the obstacles

What other major factors holds people back from achieving their wealth goals in property?

Smart asset selection is crucial, especially for the first property, as this will form the bedrock of your portfolio which allows you to go on and build equity for the second and third properties.

There’s a lot of information on this blog and picking high capital growth locations and the right property type with sustainable yields is the key to your success.

There will inevitably be ups and downs along the way, and if you took your investment cues from the mainstream media you’d never get started.

In my experience the best thing to do is start as soon as possible, choose your information sources and advisory team wisely, adjust course along the way, learn from any setbacks, and simply resolve to keep on going.

Australia is a fabulously wealthy country with a vast projected population growth for the next 40 years and beyond, so there will be plenty of opportunities to continue growing your wealth.

To have one of the friendly Propertybuyer Buyers' Agents to contact

you in regards to buying property :

or

or

call on 1300 655 615 today.

.svg)

.svg)

.svg)