By Guest Blogger, Pete Wargent,

Next Level Wealth

Rising prices in 2023

It’s a natural reaction to slow down your spending when interest rates are higher, and potentially to put off property and other investment decisions for another day.

When the largest proportion of your income is going towards your mortgage repayments, it can be hard to consider taking on more debt.

But when thinking about buying an investment property, is it a smart idea to consider ignoring the noise or buying in a counter-cyclical fashion?

It appears that property prices have increased throughout 2024 and are still rising, despite the higher level of interest rates.

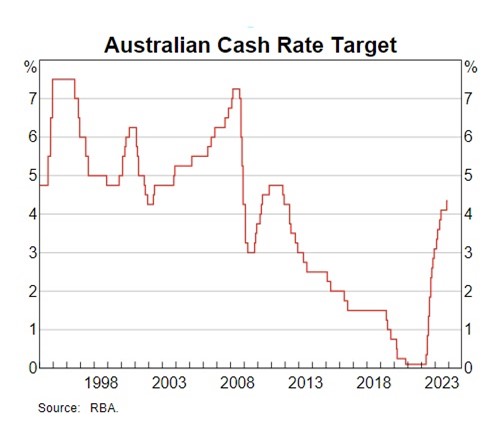

A very brief history of interest rates in Australia

Here’s a recent history of Australia’s cash rate target, which ran to above 7 per cent during the resources construction boom years, and then fell to the zero lower bound during the pandemic.

Inflation targeting in Australia was introduced in 1993, and before that time we had some periods of excruciatingly high interest rates, including in the double-digits in the early 1990s.

Since that time, on average both inflation and interest rates have been structurally lower.

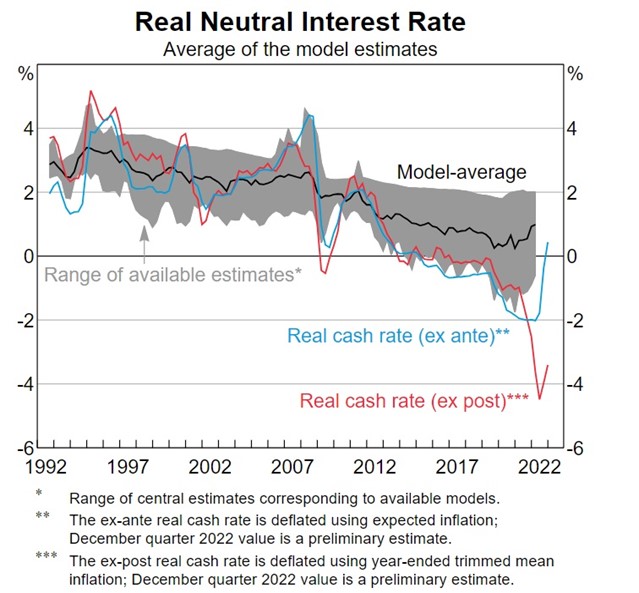

The neutral interest rate

What is the neutral interest rate? According to the Reserve Bank of Australia it is:

“…the interest rate that keeps growth at trend and inflation constant at target, when no other shocks are hitting the economy. Put another way, it is where the policy rate settles once all shocks have played out.”

Straightforward enough, but where is the neutral rate today?

Well, nobody can say for certain…. a bit like the horizon, the neutral rate might move as you get closer to it!

Australia has a nominal inflation target of 2 to 3 per cent on average, and the latest rhetoric from the central bank iterated a focus on the implied target at the middle of that range of 2½ per cent.

Different models produce a range of different results, but an average of the most prominent models out there suggest that the real neutral interest rate might be around 1 per cent (or perhaps just a touch lower).

Therefore, it seems reasonable to conclude that the neutral interest rate may be around 3½ per cent, although this figure isn’t directly observable, and we can’t say for sure.

The cash rate target today is now higher than this at 4.35 per cent, so it is likely to be a contractionary monetary policy setting, thereby slowing down inflation and the economy through 2024 (which is exactly what is being forecast by the Australian Treasury and the central bank).

Goldilocks investing

Interestingly property prices increased solidly in 2023, despite the sharp increases in mortgage rates.

The problem with waiting for everything to be just right, then, is clear.

How many periods of time in history have there been where property prices have risen when interest rates were also rising? Well, plenty!

1994, 2000, 2002, and 2005 to 2007, for example, were all periods where interest rates were being hiked, yet property prices were generally rising, at least in nominal terms (albeit not always in every capital city simultaneously).

How should a property investor think about investing when interest rates have risen so rapidly and borrowing capacity is down?

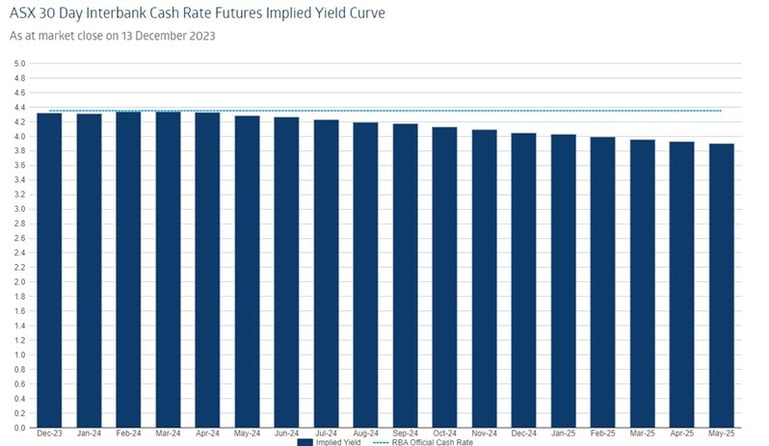

The first thing to note is that we are probably now at or around the peak of the interest rate cycle, with a couple of interest rate cuts priced in by money markets over the next 18 months.

There are some investors who always procrastinate and never take action, which is rarely ideal.

At the other end of the spectrum there are those who blindly invest as much as they can whenever they can.

Neither extreme is likely to be smart, of course!

Managing risk in 2024 and beyond

Looking into 2024, there may be more opportunities to buy from distressed vendors, particularly cashflow-focused investors, when interest rates are higher than they have been for some years.

Investors should consider maintaining a reasonable buffer, as there are sharp increases in insurance policy premiums, strata levies, trades, materials, and other costs cascading through the economy.

And of course, there’s still a risk that interest rates could go higher in the event of, for example, an oil price or geopolitical shock.

Given the lag in the full impact of the 13 interest rate rises to date, 2024 will likely more insolvencies and mortgage arrears, and a fair dose of economic pain needed to slow down spending in the economy.

One challenge for investors is that their borrowing capacity may be down from the peak by up to 30 per cent, due to the higher interest rates.

While APRA may release some of the 3 percentage points lending assessment buffer, there’s also no guarantee that borrowing capacities will increase materially any time soon.

Waiting around for easier lending policies could be self-defeating if the market continues to rise and leaves you further behind.

The outlook

There are number of factors underpinning the market in 2024.

We have record low rental vacancy rates of under 1 per cent, soaring rents, and high migration on the demand side of the equation.

On the supply side, an explosion in the costs of materials and trades is forcing thousands of construction and development firms into insolvency, and so few projects are passing feasibility that an undersupply is baked in for the next couple of years.

While some investors are offloading their least-preferred or worst-performing properties, overall stock levels remain tight, especially for quality listings.

For these reasons and more, property prices will likely record further solid increases in 2024.

To have one of our friendly Buyers' Advocate's contact you, click here to:

or

or

call us on 1300 655 615 today.

.svg)

.svg)

.svg)